Risk/Reward

Asset values fluctuate according to market conditions. Whether it is property, a business, a painting, jewellery, stocks etc... The big question is: 'how can we forecast future movements?' Forecasting future market conditions is extremely difficult, if not impossible. The logical process is to look at the past and make a professional judgement. However, the past does not guarantee the future! How then, can we make judgements of risk and potential future returns?

Risk can be divided in two: Systematic (a broad risk that markets can fall as well as rise affecting all markets) and Non-systematic (A risk specific to a particular investment relative to the market as a whole) risk.

The amount of risk we can tolerate depends on a number of factors. Your objectives, term, type of investment etc, play a crucial role. However the main judgement is usually dictated by your personality - your risk profile. If you are the type of person who has trouble stomaching a loss, then stocks and similar investments are too much risk. If, however, you prefer your money to grow and are happy to take some risk, then they may be suitable. The old saying: 'to accumulate, you have to speculate' is a valid one. Of course, the words accumulate and speculate can have different meanings to different people. For example, to one person it might mean making or losing only 5 to 20% and to someone else it might mean gaining or losing up to a 100%.

No one is alike and at Trinity Holdings, we make sure that we understand each individual clients expectations and tolerance of risk before making recommendations. Our Financial Health Check includes a question on your risk profile.

To be able to get your investments (your portfolio) in the blue box or close as possible, you can depend purely on luck or apply the Principles of Portfolio Construction. The purpose of these principles is to minimise risk and potentially maximise returns according to the individual investors objectives, within the risk/return relation. Risk cannot be completely eliminated, but can be reduced by applying diversification.

Referring to the above graph, an asset's investment risk can be measured through its past performance. All major funds with at least a three-year history will have a Standard Volatility figure. Checking the fund's volatility is an important factor when coming to make an investment decision. It shows its past performance over a period (usually three years) over its volatility/risk calculated as Standard Deviation. (A statistical measure of the degree to which an individual value tends to vary, how much it moves up or down, from it peers.)

Another important factor is the correlation ratio of various assets within a portfolio. (Correlation is not used as a measure of risk, but to reduce the overall portfolios risk).

For example, there are a number of investments that produced in excess of 50% returns during 2002. However, the opposite exists as well, where they have fallen. In most cases if one type of investment (market) produces big returns, and the other one does not, it could mean that their assets are negatively correlated or non-correlated.

For example, when the US Dollar value falls, gold usually goes up and vice versa. Therefore, they are usually negatively correlated.

Or, in the past three years stock markets have fallen, but managed future funds and hedge fund have performed impressively. And during the 90’s the stock markets were extremely bullish and managed futures and hedge funds performed positively at a lower rate. Therefore, we can say that these two assets have little or no correlation. In other words, one asset can go up or down regardless of the other asset movements.

By using Standard Volatility to measure Risk and using Correlation to measure similarity of asset movements, one can produce a balance portfolio to potentially protect it from different unexpected trend moves.

There are many ways of measuring risk. Other methods include the Sharpe Ratio, the Sortino Ratio and the MAR Ratio.

*Please note the ratios are based on the past only and do not guarantee the future

Disclaimer: This advice is general and based on our current understanding of UK law and Inland Revenue practice in relation to individual residents outside the UK. They are not specific to residents of any particular country. Individual advice is essential in all cases. Levels and bases of, and reliefs from, taxation are subject to change, tax rates and reliefs referred to are those currently applying the UK and their value depends on the individual circumstances of the investor.

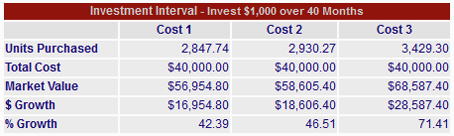

Cost Averaging

Cost Averaging (often called Dollar Cost Averaging) is a method of accumulating assets by investing a fixed amount of money in securities at set intervals. The investor buys more shares/units when the price is low and fewer shares/units when the price is high; the overall cost is lower than it would be if a constant number of shares/units were bought at set intervals.

This method can be applied to investments on a regular basis, or by investing a single lump sum investment and slowly feeding it from low risk to higher risk fund/s, known as Phased Investment Switching.

The below graph is an example only and it is showing investments over a period of 40 intervals. The red graph shows an ideal investment constantly growing. The blue and the green represent fluctuating investments.

|

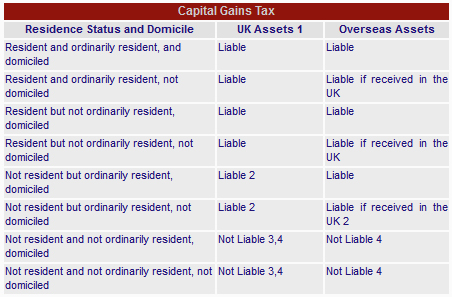

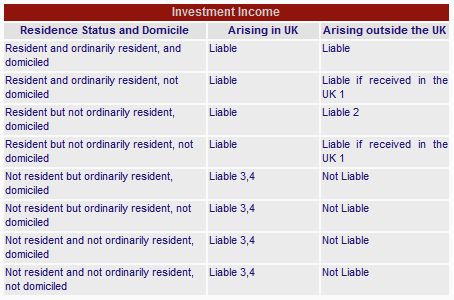

United Kingdom Taxation This page is for persons who might be affected by UK Tax. It shows general limited information on UK Tax treatment, depending on an individual's residence and domicile. The facts are based on Trinity Holdings understanding and are given for consideration only. For specific information, please contact us. An individual’s residence and domicile status is important when determining his or her liability to UK Tax. Residence Ordinary Residence Domicile  1. You are taxable on the whole of the income arising in the Republic of Ireland.

1. There is no liability if the disposal is of certain UK Government Securities

|

|

Consultation + Research + Advice + Action + Commitment = Total Financial Planning